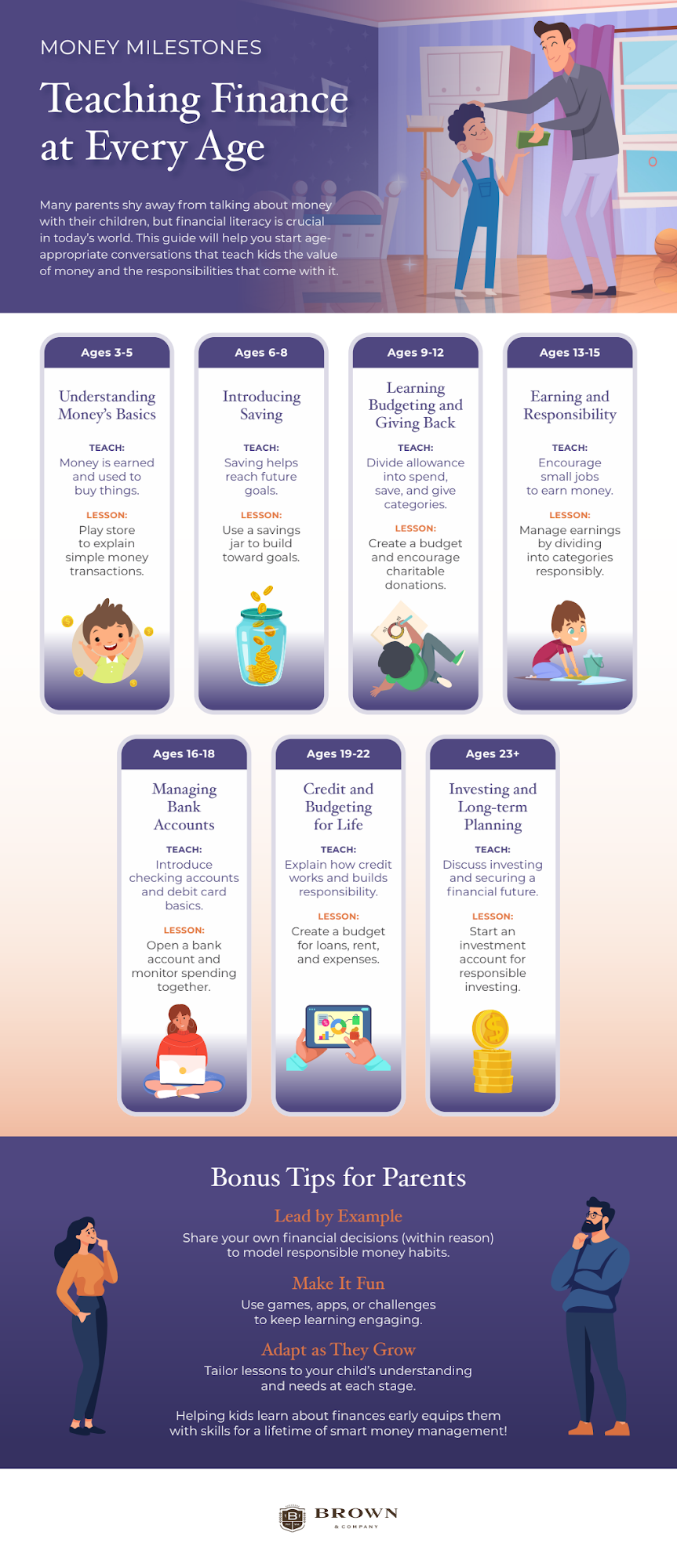

Financial literacy is a crucial life skill that should be taught at every stage of life. By instilling financial principles early and reinforcing them throughout different phases of life, individuals can build a strong foundation for economic security. Additionally, estate planning—often overlooked—is an essential aspect of financial education that ensures long-term financial well-being. Below is a guide on how financial education should evolve at various life stages.

Childhood (Ages 5–12): The Basics of Money Management

The earlier children are introduced to financial concepts, the better their chances of developing healthy money habits. At this stage, parents and educators can focus on foundational concepts such as:

- The value of money: Understanding different denominations and their purchasing power.

- Saving vs. spending: Introducing piggy banks or savings jars to show how money accumulates.

- Earning money: Encouraging small tasks to earn an allowance fosters a work ethic.

- Needs vs. wants: Helping children distinguish between essential expenses and luxury items.

Simple estate planning discussions can begin by explaining the concept of inheritance in a simplified way, such as how belongings can be passed down in a family.

Teenage Years (Ages 13–19): Budgeting and Smart Spending

Teenagers should start taking more responsibility for their financial decisions. At this stage, financial education should include:

- Budgeting: Teaching how to allocate income from allowances or part-time jobs.

- Bank accounts: Encouraging opening a savings account to learn about deposits and withdrawals.

- Credit and debt: Explaining the basics of credit scores, interest rates, and the dangers of accumulating unnecessary debt.

- Investment basics: Introducing simple investment vehicles like mutual funds or stocks.

Estate planning lessons at this age can involve discussing the importance of wills and why families plan for the future to ensure financial stability.

Young Adulthood (Ages 20–35): Building Wealth and Financial Independence

This phase is critical for making financial decisions that impact long-term stability. Key financial lessons include:

- Emergency funds: Setting aside three to six months’ worth of living expenses.

- Retirement planning: Understanding employer-sponsored plans like 401(k)s and IRAs.

- Debt management: Developing strategies to pay off student loans and credit card debt.

- Homeownership: Learning about mortgages and saving for down payments.

- Insurance: Recognizing the need for health, life, and disability insurance.

Young adults should also be encouraged to start basic estate planning by naming beneficiaries for financial accounts and considering a simple will.

Midlife (Ages 36–55): Protecting and Growing Wealth

This stage focuses on securing and expanding financial assets while preparing for the future. Financial priorities should include:

- Maximizing retirement contributions.

- Investing in diverse assets to build wealth.

- College savings plans for children (such as 529 plans).

- Estate planning: Drafting a comprehensive will, establishing trusts, and appointing a power of attorney.

Estate planning becomes crucial at this stage, ensuring that assets are distributed according to one’s wishes and that dependents are protected financially.

Retirement and Beyond (Ages 56+): Wealth Preservation and Legacy Planning

As retirement approaches, financial education should focus on sustaining income and estate management. Important considerations include:

- Withdrawal strategies to ensure retirement savings last.

- Tax-efficient investment management.

- Long-term care and healthcare planning.

- Estate planning updates: Reviewing wills, trusts, and designating healthcare proxies.

Estate planning at this stage solidifies one’s financial legacy, ensuring smooth transitions for heirs and beneficiaries.

Final Thoughts

Teaching finance at every stage of life is essential to fostering financial security and responsible money management. Incorporating estate planning into financial education ensures that individuals not only secure their own financial future but also pass on a legacy of financial stability to future generations. By taking a proactive approach, people of all ages can build a strong, sustainable financial foundation that lasts a lifetime.